MARCH 2026

ISSUE 06

AIG QUARTERLY

A Resurgent London

_______

Auctions and Exhibitions Impress

Against a volatile geopolitical backdrop, the first major series of auctions this year in London set an upbeat tone that defied expectations. During the recent market downturn, modern and contemporary sales in Europe and Asia have been impacted by the difficulty of attracting high-quality material, with discretionary consignors either waiting for an uptick, or leveraging their position to secure lot placement in marquee New York sales. This season upended this trend: both the palpable energy on the ground and the sale data firmly pointed to a resurgence in activity in Europe’s art capital. The major auction houses recorded outsized results compared to the year previously: Christie’s realized £245.2m ($329.9m) across evening and day sales, a 72.9% increase; Sotheby’s posted £154m ($206.8m), a 94% rise.

Such strong results are especially compelling given the tumultuous international environment. The weekend prior to the auctions, America and Israel struck Iran, catalyzing a continuing wave of attacks across the Middle East. As many expected, military action has provoked a period of extreme volatility in global financial markets as investors assess the potential of long-term economic disruption. Not impervious to the wider situation, collectors nonetheless came out in force – notable bidding wars pushed rare, desirable material towards new heights. Sentiment was especially strong for Modern British artists, a segment of the market long stable but – except for a few notable exceptions – largely having missed out on the explosive growth American contemporaries have experienced over the last thirty years. An exceptional and rare canvas by Leon Kossoff, Children’s Swimming Pool, 11 o’clock Saturday Morning, August (1969), was one of two works from the artist’s landmark Swimming Pool series remaining in private hands. Where Kossoff works are usually found in more regionally focused British Art sales, this painting benefitted from its recontextualization within the Lewis Collection. Presented in both New York and London alongside three canvases by Francis Bacon and Lucian Freud, the work was viewed in the same space as two artists established in marquee evening sales. Sotheby’s extensive marketing of the painting was richly rewarded: despite being the lowest value lot in the Lewis consignment, a £5.2m ($7m) result – nearly nine times its low estimate – was the highlight of the night.

Healthy demand for British artists was felt elsewhere, too. Bacon’s self-portrait and two delicate Freuds from the Lewis Collection each performed well, while Henry Moore’s King and Queen (1952-53) achieved a new auction record for the artist at £26.3m ($35.4m); a large Barbara Hepworth sculpture also made £3.5m ($4.7m). This slate of Modern British lots in the seven-figure and low eight-figure range was complemented by a strong supply of European material on offer. Historically established European artists of the post-war period continue to hold an attractive value proposition relative to their American peers. The auction houses prioritized well-priced, mostly fresh-to-market property by such figures, which led to strong results for the likes of Michelangelo Pistoletto, Jean Dubuffet, Gerhard Richter, Lucio Fontana, Eduardo Chillida, Alberto Giacometti, Anselm Kiefer, Joan Miro, Paul Delvaux, and Dorothea Tanning, among others. At a time of global uncertainty, established blue-chip names sourced from notable collections in Europe proved attractive to collectors; even if these works are unlikely to produce blockbuster returns, they appeal both as an asset – safe, inflation-hedged stores of value – and psychologically, offering an opportunity to connect with the past inventions of humanity during troubling moments past and present.

Henry Moore, King and Queen (1952-53)

Notable Auction Results

ALBERTO GIACOMETTI

Femme debout (c.1960)

Sotheby’s, Modern Evening Sale

4 March 2026

Estimate: £2,200,000 - 2,800,000

Sold: £5,092,000 ($6,832,980)

JOAN MIRÓ

Peinture (1949)

Christie’s, Art of the Surreal Evening Sale

5 March 2026

Estimate: £1,500,000 - 2,500,000

Sold: £4,808,000 ($6,451,879)

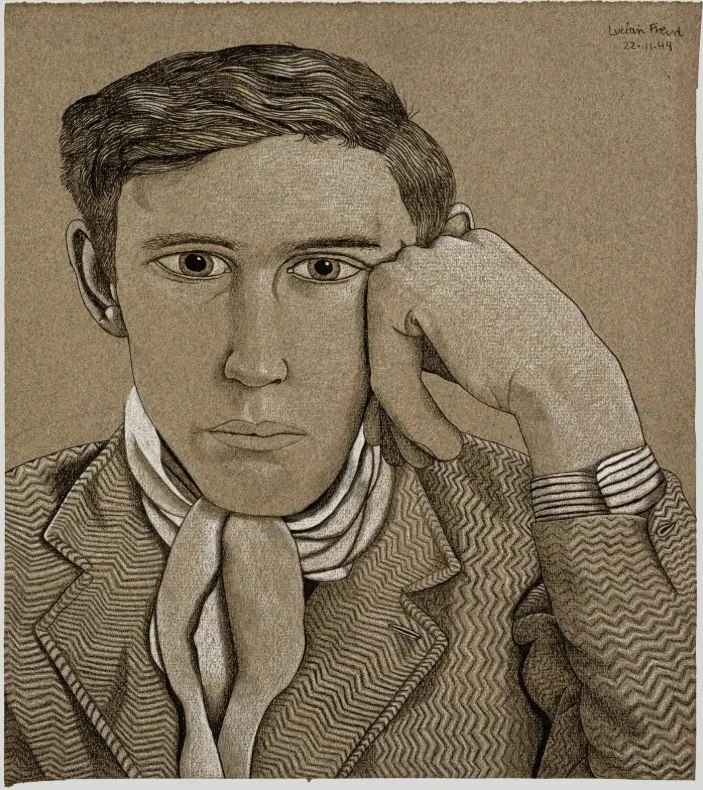

In addition to London’s wealth of specialist expertise and established market infrastructure - factors that certainly contributed to its resurgence this season - the city continues to boast a dynamic, highly developed institutional landscape, whose focus of late has highlighted homegrown artists, both historical and contemporary. A major John Constable / William Turner exhibition at Tate Britain explores the rivalry between two stalwarts of British art history, both of whom were pivotal to the seismic evolutions in European painting later in the century (up through 21 April). Meanwhile, the National Portrait Gallery has just opened an impressive Lucian Freud show, which, judging by the overwhelmingly positive reception, was not lost on potential bidders in this past week's sales. Taking the vantage point of Freud's draftsmanship as foundational to the artist's singular painting style, the exhibition is a riveting, mini retrospective (up through 4 May). A force to be reckoned with since her debut in the 1990s, Tracey Emin has staged an ambitious, visceral exhibition at the Tate Modern, which opened two weeks ago to the toast of the London art world and beyond. Entitled A Second Life, the show is a groundbreaking survey of the artist's transgressive career, showcasing the tender, confessional, and at times heart-wrenching work of an artist who continues to define our times (up through 31 August). Finally, Cecily Brown will present a suite of new paintings alongside older hits at the Serpentine Gallery later this month, hot on the heels of Peter Doig’s hugely popular display at the same venue. It will be the first major painting show of the artist in the UK in over twenty years and represents something of a homecoming for the British-born, New York-based painter (27 March through 6 September). Together, these exhibitions underscore how native artistic movements – from the London School to the YBAs, and a painting tradition stretching back to the Romantic era – continue to captivate audiences, while reaffirming London’s position as a vital platform for exploring cultural heritage.

The gallery scene in London remains active, with key dealers redoubling efforts after what many consider to be the successive blows of Brexit, the pandemic, and most recently, the government’s non-domicile tax reforms. Despite these headwinds, gallerists continue to reinvent themselves and, in doing so, demonstrate the staying power for the city as a major center for the production, exhibition, and exchange of contemporary art. Sadie Coles HQ opened a palatial new space on Saville Row late last year with a significant Lisa Brice exhibition, followed by a whimsical group show this spring based on an Oscar Wilde novella. Modern Art also moved to a grand new gallery in St. James late last year, consolidating a handful of smaller spaces; Maureen Paley, Grimm Gallery, and Skarstedt have also all opened new or enlarged spaces in the past twelve months. A crop of younger gallerists has found footholds in the city, initiating a collaborative, artist-led atmosphere that is engaging younger audiences and breathing fresh life into a beleaguered contemporary market. In the face of Paris’s momentum, bolstered by the arrival of Art Basel fair now held in the city, London’s position as Europe’s art-world capital still looks difficult to dislodge.

Tracey Emin at Tate Modern. Photo: Sonal Bakrania

Looking Ahead: Art Basel Hong Kong

Later this month, attention turns to the 2026 iteration of Art Basel Hong Kong, the marquee event in Asia’s art world calendar. Now in its thirteenth edition, the fair continues to be in-demand and oversubscribed; for most participating galleries, keen to leverage the premier position of Art Basel’s platform, the week marks their principal point of contact with Asian collectors. 32 first-time exhibitors will feature, bringing the total to 240 participants. Curators from the region – Mami Kataoka, Isabella Tam, Alia Swastika, and Hirokazu Tokuyama – will be highlighted in the fair’s ‘Encounters’ section; the popular digital art initiative, ‘Zero 10’, will also return after its thought-provoking spectacle in Miami Beach.

Galleries enter a more sophisticated collecting landscape than that found at earlier editions of the fair. The recent period of market downturn – most pronounced in the contemporary segment – has hastened the move away from rapid acquisitions of young, in-demand artists, driven by a fear of missing out or the possibility of speculative financial gains. Now, a ‘second chapter’ has emerged: collectors in the region are investing more time into research, seeking expert advice, and becoming more selective before committing to purchases. The whirlwind opening day pace of past years is unlikely to recur later this month; long-term thinking and a growing predilection towards established, blue-chip names are re-defining a maturing collector base in Asia.

The auction houses will also stage a series of sales during the week, marking only the second sales week in Hong Kong staged from the three houses’ own headquarters during ABHK. This is particularly salient logistical point: previously, auction previews had to be installed at the convention center, which was unavailable in March as it also hosts the fair. Specialists will be hoping that momentum from the strong London sales earlier in the month will carry forward in what constitutes the last major market test before May’s marquee sales in New York.

Hong Kong’s cultural leadership has been adept at capitalizing on the art world’s focus over the week of ABHK, not only highlighting the region’s art market but also the growing footprint of its cultural institutions. In the last few years, major museum conferences have been held to coincide with the fair, a trend set to continue in 2026. At the HK International Cultural Summit, leading museum executives including the Director and CEO of the Solomon R. Guggenheim Museum, New York, the new Director of the Museum of Modern Art, New York, and the Director of the Uffizi, Florence, are set to speak. Notably, a number of museum figures from outside the West – China, India, Saudi Arabia, United Arab Emirates, Senegal, Brazil, Thailand, Australia – are also slated to participate, reinforcing the important role Hong Kong has to play in developing and diversifying the international museum landscape.

The event will take place amidst a backdrop of recent additions to Asia’s institutional landscape ecosystem. Over the winter months, a wave of new private art museums and foundations across China and Southeast Asia have either opened or been announced. Dib Bangkok (which holds the only site-specific James Turrell structure in Thailand) and the H+ Museum in Suzhou both staged their inaugural exhibitions in December with collection displays combining international and local artists; last month, Chinese technology titans Tencent and JD.com unveiled plans to each construct art galleries within their expansive new campuses in Shenzhen; and in Singapore, the recently incubated Tanoto Art Foundation and Kim Association staged exhibitions during ART SG in January.

Dib Museum, Bangkok. Courtesy of Dib Museum

In China, where museum sites founded by wealthy entrepreneurs have become a fixture over the last two decades, private institutions are being afforded more space to experiment with traditional museum operations. Reflecting on how the museum ecosystem has evolved in recent years, Robin Peckham – the recently appointed Executive Director of the forthcoming JD Museum – identifies a new dynamic between public and private institutions. Speaking exclusively to Art Intelligence Global, he notes how, in the last few years, ‘the emergence of state museums for contemporary art as serious players in mainland China’ – such as the New Guangzhou Art Museum (2023), the Bai’etan Greater Bay Area Art Center (2023), or the Suzhou Museum of Contemporary Art (opening later in 2026), to name a few – ‘eases the heavy sense of responsibility that smaller, privately founded museums carry.’

With public museums increasingly platforming contemporary art, greater space is being afforded to new institutions to capitalize on their incubation as a blank slate, primed to embrace innovative display strategies and modes of audience engagement. For Peckham, this means ‘We can now function more like a laboratory’, one in which the gallery is ‘simultaneously a magical, ritual space and a part of the neighborhood’, cultivating dialogues with local audiences with whom the city is shared.’ These spaces can also pivot their curatorial programming towards prescient contemporary concerns that appeal to new audiences. In the case of the JD Museum, ‘questions surrounding the human experience of technology’ will be mission critical, says Peckham. ‘We want to create a space for sitting with these questions in a constructive way’, a goal which museums in the West have thus far largely struggled to achieve.

With the pulling power of Hong Kong on full display at the end of the March, it is unlikely that the city will be replaced anytime in the near future as Asia’s international cultural hub; like London, concerns about the city’s premier position on the art market calendar a few years ago seem to have been premature. Moreover, the considered inclusion of wider museum discourse during the region’s principal art week is a smart, forward-thinking practice that augments concurrent infrastructural growth, provoking greater integration between new Asian institutions and the global museum community. Against the backdrop of dominant demographic trends in South-East Asian countries, this necessary shift will only become more important in years to come.

A rendering of the forthcoming JD Museum. Courtesy JD.com

Upcoming at AIG Hong Kong

Yayoi Kusama, Driving Image, 1964-66. © YAYOI KUSAMA

THE UNCANNY

21 March - 15 May 2026

Opening Reception: 24 March 2026 (5-8PM)

Suite A, 1/F, TS Tower

Heung Yip Road, Wong Chuk Hang

Art Intelligence Global is pleased to present “The Uncanny”, opening on 21 March 2026 at our Hong Kong gallery space. Coinciding with Art Basel Hong Kong, “The Uncanny” explores how artists render the familiar strangely unsettling, interrogating the self as a site where desire, memory, and anxiety converge. The group exhibition will includes historic works by Yayoi Kusama, Robert Gober, Sarah Lucas, Cindy Sherman, Nam June Paik, and Salvador Dalí, among others.

Exhibition Recommendations

17 March - 28 June 2026

Hoam Museum of Art, Yongin

Through 31 May 2026

The Jewish Museum, New York

Lucian Freud: Drawing into Painting

Through 4 May 2026

National Portrait Gallery, London

Copyright (C) Art Intelligence Global, 2026.

All rights reserved.

Reach us at:

32 E 57th Street Floor 12

New York, NY 10022 USA

Suite A, 1/F, TS Tower

No. 43 Heung Yip Road, Hong Kong

info@artintelligenceglobal.com